Measures announced

On 7 September 2012, the Portuguese Government announced new austerity measures that include an increase (of 7 percentage points) in the contribution of workers towards social security together with a decrease (of 5.25 percentage points) in the contribution of companies. This would place Portugal broadly in line with Germany. The first measure was aimed at fighting the increased cost with social security and generally to help achieve the new deficit goal, agreed with the ECB, EU Commission and IMF. The second measure taken was aimed at providing companies with sufficient funds (savings from the tax break) to keep jobs and foster employment.

Impact on the economy

This measure should help support the social security accounts that are suffering badly from the rise in unemployment. Moreover, the Government expects that this measure will support employment and increase competitiveness for firms (according to finance minister Vitor Gaspar, this measure will create 1 to 2% employment by 2015), as a result of lower costs for employers. However, these effects are unlikely to have a significant impact in the short run. A recent study by four economists from the University of Minho revealed that the net effect of measures will actually increase the unemployed by 68 thousand. The economic outlook remains sharply recessionary for Portugal, and cloudy for most of Portugal’s trading partners. This scenario is not favorable for the predictions made by the government.

Reactions

Reactions to the announcement of these austerity measures were widespread and predominately negative. In Portugal, business leaders rose against the measures saying they were unnecessary and will not benefit their companies. Paulo de Azevedo from Sonae, one of the largest business groups in Portugal, claimed that these measures would be harmful for non-exporting companies. The announcement also shook the political sphere with the opposition and even some members of the Government party (PPD/PSD) opposing and criticising the measures. The coalition that enabled the government to have majority in the Portuguese parliament was weakened with the head of CDS/PP publicly admitting to be against the measures.

Source: Bloomberg

Investors’ reaction was ambiguous or indifferent as we can see that from the chart above. It shows the yield to maturity of Portuguese 10 year government bonds and its evolution last month. The first drop which occurred on 5 of September was an obvious positive reaction to the ECB’s announcement of its intention to purchase sovereign debt from struggling countries. However, the reaction after the announcement of these measures (on 7 September) was negative, at first glance. However, it is hard to isolate the effect, due to a high number of relevant events that might have also affected the yield. It is unclear whether the markets are factoring in one of the largest demonstrations in the history of the country having taken place during the weekend.

The European Commission admitted that the government could drop the measures if it could come up with an alternative to fulfill the adjustment programme’s goals as agreed with the IMF. A year ago, IMF representatives alerted to the risks of these measures and their intended purpose. The delegates believed that “it is not obvious that promoting employment is a good substitute for increased efficiency”. Moreover, the head of the IMF delegation, Adebe Salassi, recently stated that these measures were not enforced by the delegation and were solely an initiative of the Portuguese government.

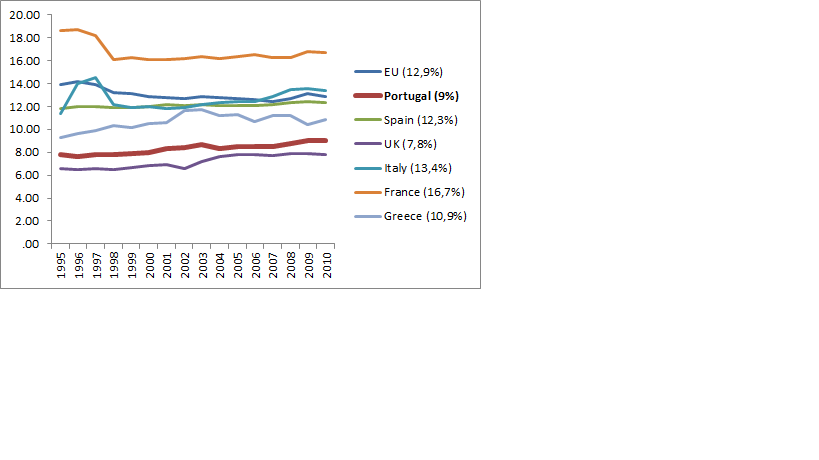

As these measures are likely to affect the contributions to social security in Portugal, we find it relevant to compare these with other European countries. Looking at the overall map of aggregate contributions of employees and employers for the European Union countries as a percentage of GDP until 2010, we find that Portugal is below other countries in terms of contributions and is closer to the UK than to other southern European countries such as Spain or Italy, for example.

Source: Eurostat

Innovation Models insight

Here at innovation models, our opinion/reaction about this measure is also mixed. Had Government announced that the proceeds from the reduction in employer contributions were directed at developing innovative projects that might foster employment in the long run, we would consider these measures as positive. This would have been difficult to implement anyway. We believe that the source of the economic difficulties in Portugal has not been addressed yet.

This matter was discussed in ETV’s “Closing Bell” programme on 18 September (in Portuguese):

{kind=link}

{kind=link}