We spend a lot of time discussing the need to cut Government debt. While this is legitimate, we keep forgetting that in every 6 SMEs in Portugal, one has failed its debt repayment or interest payment obligations.

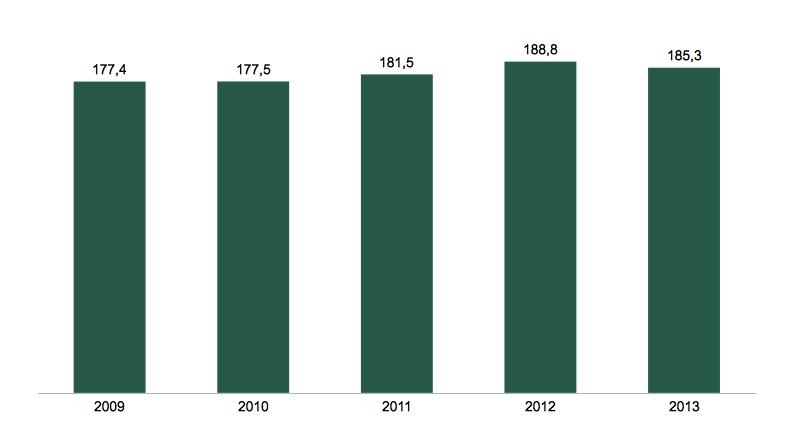

If you think that companies are adjusting to the crisis by reducing their debt, think again. The debt/GDP ratio for private, non-financial companies was on the increase until 2012 and only recently has there been a change in this trend.

Debt of non-financial private companies in Portugal as a % of GDP, 2009-2013. Source: Bank of Portugal (2014)

Debt of non-financial private companies in Portugal as a % of GDP, 2009-2013. Source: Bank of Portugal (2014)

The difficulty here is that this lack of credit creates a bottleneck for the financing of innovative projects. The credit market has been affected by the economic crisis. The main problem of the commercial banks is to restrict the concession of credit at all costs, to manage their loan portfolio. This means that innovative companies are unable to get access to bank credit to finance their expansion. It is difficult for the banks’ existing clients to draw credit, let alone for new projects which are inherently risky.

Sources of financing for a sample of start-ups based in Lisbon (2014). Source: Macrometria

Sources of financing for a sample of start-ups based in Lisbon (2014). Source: Macrometria

In a recent survey, Macrometria found that bank financing accounts for 2.8% of total financing sources for a representative sample of start-ups in Lisbon. As banks seek to cut their credit exposure, and existing funds are used to re-finance over-indebted companies, the true losers are start-ups and ultimately, innovation itself.

On the other hand, bank debt is not being used to finance start-ups and this can be seen as a positive. The current business culture relies excessively on debt. The next stage of recovery will be sustainable if companies learn how to grow using equity. If the excessive levels of debt as a source of financing were one of the reasons for the anemic growth of the last decade.