The Portuguese film industry is an example of the difference between creativity and innovation. Portuguese films fail to attract audiences even in their home market, let alone internationally. With dwindling public funds to finance productions and fierce competition, prospects are not bright to say the least.

A total of 23 films were produced in Portugal in 2011. Ten of those had fewer than 500 viewers. The others typically achieved less than 10,000 and only a couple managed to attract audiences around 20,000. This is a dismal track record by any standard. Why were these pictures unsuccessful?

There are four stages in the innovation process: ideas, insights, invention and innovation. Everyone has ideas. If you share your idea, it may become an insight. If your insight is turned into a product (or service) it becomes an invention. Finally, if that invention is successful in the market, this makes up innovation.

"Innovation means selling tickets"

Films (or documentaries) are often based on new ideas and insights and original scripts – a product of creativity. In my opinion, the right measure for judging whether a film is innovative (not just creative) is public acceptance. If a film is creative and manages to attract large audiences, this is an innovation. Having good reviews is not enough.

Note that the reverse is not necessarily true: public acceptance does not always stem from innovation. Most Hollywood blockbusters are not innovative at all. Instead, they are based on small, incremental variations on a well-known genre. Looking at 2011 global box office results, the top 7 films are sequels.

Back to Portuguese film production, I am willing to accept that at least part of the 23 films produced in 2011 involved some creativity, new insights or original scripts. What prevented these films from reaching larger audiences? I confess that have not seen any of them, but I am willing to take a guess.

The first potential barrier is that Portuguese cinema production is State-financed, to a large extent. Both State and local authorities spend a considerable amount of cash to finance films and promote them. Financing films using public funds has various drawbacks. Among others, a committee has to decide which films are worthy of support. Decision by committee is a known innovation killer.

Another barrier is viewer education. The Portuguese population has a relatively low-level of education compared to most European countries and to draw audiences, films have to be simple – perhaps too simple. Lack of education acts as a constraint on innovation.

Foreign markets could give additional audiences but in fact, Portuguese-spoken films do not seem to be easily exportable. Brazilian audiences have to make an effort to understand the language as it is spoken in Portugal.

Hollywood studios are the dominant force in the industry, shaping audience preferences. Hollywood has developed an ability around simple films, based on familiar genres.

The difficult economic conditions and large State deficit will create more difficulties. The Government’s budget for 2012 specifically identifies cinema as one of the areas where the State will review its policy. This will almost certainly involve spending cuts.

Is there any way to overcome these barriers?

The obvious choice would be to produce films for mass consumption. However, cinema production and direction is a complex eco-system. It is questionable whether directors working in Portugal are interested in reaching large audiences. In fact, the most successful film of 2011 (in terms of audiences) was João Canijo‘s “Sangue do meu sangue“, describing the harsh realities of a family living in a slum in the outskirts of Lisbon. Tough subjects seem to be the norm.

With limited audience acceptance, reduced State budgets and strong competition, the future does not look too good for Portuguese cinema production. Yet it is essential that the industry continues to exist as it encourages pluralism, creativity and diversity.

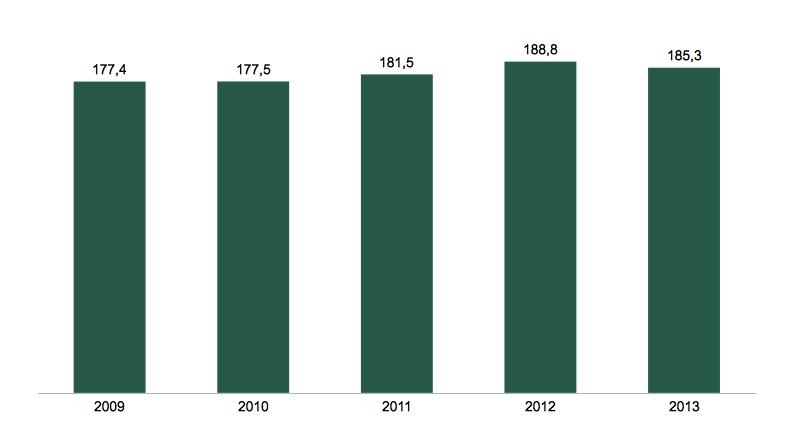

Debt of non-financial private companies in Portugal as a % of GDP, 2009-2013. Source: Bank of Portugal (2014)

Debt of non-financial private companies in Portugal as a % of GDP, 2009-2013. Source: Bank of Portugal (2014) Sources of financing for a sample of start-ups based in Lisbon (2014). Source: Macrometria

Sources of financing for a sample of start-ups based in Lisbon (2014). Source: Macrometria