We spend a lot of time discussing the need to cut Government debt. While this is legitimate, we keep forgetting that in every 6 SMEs in Portugal, one has failed its debt repayment or interest payment obligations.

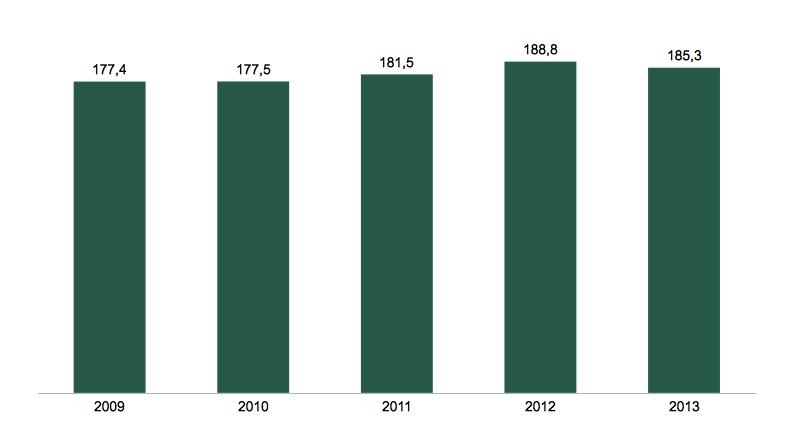

If you think that companies are adjusting to the crisis by reducing their debt, think again. The debt/GDP ratio for private, non-financial companies was on the increase until 2012 and only recently has there been a change in this trend.

Debt of non-financial private companies in Portugal as a % of GDP, 2009-2013. Source: Bank of Portugal (2014)

The difficulty here is that this lack of credit creates a bottleneck for the financing of innovative projects. The credit market has been affected by the economic crisis. The main problem of the commercial banks is to restrict the concession of credit at all costs, to manage their loan portfolio. This means that innovative companies are unable to get access to bank credit to finance their expansion. It is difficult for the banks’ existing clients to draw credit, let alone for new projects which are inherently risky.

Sources of financing for a sample of start-ups based in Lisbon (2014). Source: Macrometria

In a recent survey, Macrometria found that bank financing accounts for 2.8% of total financing sources for a representative sample of start-ups in Lisbon. As banks seek to cut their credit exposure, and existing funds are used to re-finance over-indebted companies, the true losers are start-ups and ultimately, innovation itself.

On the other hand, bank debt is not being used to finance start-ups and this can be seen as a positive. The current business culture relies excessively on debt. The next stage of recovery will be sustainable if companies learn how to grow using equity. If the excessive levels of debt as a source of financing were one of the reasons for the anemic growth of the last decade.

The Portuguese Government is about to announce increases in civil servants’ wages between 2015 and 2020.

The IMF, European Commission and European Central Bank are about to complete the adjustment programme and meanwhile, the President has declared that he would welcome an increase in the civil servants’ wages in the coming years.

Government appears to be leaning towards an increase in wages, in line with the President’s opinion. This demonstrates concern over the upcoming European elections in May 2014 and Parliamentary elections in 2015.

Increasing civil servants’ pay could potentially result in lower corruption levels, as motivated and relatively well-paid civil servants would have a lower tendency to accept bribes. However, a number of arguments can be made against any increases in civil servants’ wages at this stage:

A number of cuts in the wages of civil servants were proposed from 2008 onwards but the Constitutional Court blocked their implementation. As a result, unit labour costs are back at 2008 levels in the public sector, while there has been a decrease unit labour costs in the private sector. From this perspective, nothing has changed since the beginning of the crisis, for civil servants.

Any increase in wages would have to be justified with improvements in services provided by the State. However, there is evidence that the public is not satisfied with the level and quality of services provided. In its 2013 report (Third European Quality of Life Survey – Quality of society and public services), the European Foundation for the Improvement of Living and Working Conditions finds that the perceived quality of public services in Portugal is well below European average.

Source: Eurofound (2013), Third European Quality of Life Survey – Quality of society and public services, Publications Office

of the European Union, Luxembourg

I do not mind paying civil servants well, as long as I receive a good service in return. The main problem is the low perceived quality of public services in Portugal and from this perspective, increasing wages does not make any sense at this stage.

Whenever a company faces financial trouble, one of the first restructuring measures is to cut the number of non-core subsidiaries. Company restructuring is about specialisation: a business with negative operating income usually needs to make what sells and drop everything else.

A similar approach could be taken by the Portuguese Government to limit spending and improve the country’s public accounts. Following a prolonged period of low GDP growth (or recession) and very high Government debt (128% of GDP and growing), there is a pressing need to cut the size of the State.

Yet, almost 2 years following the intervention of the IMF, ECB and European Commission, the major tangible results of the so-called restructuring measures imposed by the country’s main lenders were a reduction in the wages of civil servants and pension cuts. Any improvements in the State’s efficiency remain to be seen.

Improving efficiency means cutting costs and this could be achieved in a number of ways. The most obvious fix is to cut salaries, which is what Government did so far. More cuts are likely in 2014, after the European Parliament elections in May. Any serious Public sector restructuring should also involve a reduction in the number of institutes, independent entities and associations that are financed using Government money. One estimate places the total number of Government and Quasi-government entities at over 13.000, for a country with under 10 million inhabitants. These are estimates since not even the Bank of Portugal knows for sure. In fact, no-one appears to know – a tell-tale sign that restructuring is badly needed.

Yet this is not likely to happen. Everyone now understands how things will turn out: there will be no fundamental reforms, nor will the State’s efficiency improve. A significant reduction in the number of State entities is not strictly needed, and will not be executed. The political system as we know it would have to change dramatically. No-one in the political arena really wants that to happen.

All that is strictly needed is to cut wages and pensions, transfer a massive amount of debt from the balance sheets of certain banks to the ECB – and that is it. Economic miracles happen in Hollywood. Around here? We will probably go back to the usual muddle-through economy. It will go according to plan.

Ever since the country went into financial assistance mode, the Portuguese Government has cut costs essentially by reducing wages and pension benefits. Why is it so hard to admit that, inevitably, some Government institutions are less efficient than average and less efficient than in other European countries? Would it not make sense to conduct some benchmarking and implement reforms?

There is a pressing need for efficiency improvements and this would almost certainly involve merging the significant amount of small institutes, independent entities and regional authorities that were created in the past 20 years.

Hopefully for the better…

The advantages would far outweigh the disadvantages: fewer needless consulting committees, boards, and commissions. Increased efficiency, leaner organisations employing more qualified civil servants would all result in sustainable cost savings.

This Government’s stated aim of tapping financial markets ASAP could create the wrong incentive. This need for speed could well become a way to avoid deeper reforms which would result in a leaner Government sector.

Are there any alternatives to the measures currently being implemented by the Portuguese Government under the supervision of the IMF, the Commission and the European Central Bank? The actions implemented up to date amount to an increase in taxes and cuts in civil servants’ pay and pension costs. While this is an effective way to make sure that the country can meet its debt obligations, little is being done to increase Government’s efficiency.

Current estimates show that 12,000 entities can carry out public procurement (according to OPET). That compares to about 800 in Ireland. In 2013, Government entities spent an estimated 15 billion euros in the acquisition of goods and services to third parties (similar to operating expenditure in company accounting). This represents roughly 20% of total Government spend. A simple 5% reduction in this expenditure would cut costs by 750 million euro on an annual basis.

How can this be achieved? It would almost certainly involve merging the plethora of institutes, regional entities, hospitals and other institutions. In Portugal, nearly every State-run hospital is a standalone company, as is every school. It would also involve using electronic procurement platforms in a more efficient way. Local Government and indeed political parties would have to adapt to this new reality.

The Portuguese Government’s 2014 budget is being discussed in the so-called “specialised” committees in parliament. The budget approval process consists of 3 steps: first, a “big picture” version of the budget is approved by Parliament- this was done at the end of October. Second, representatives of parties with a seat in the National Assembly discuss the budget in more detail. The representatives are organised in various committees (the so-called commissions) which are mandated to discuss specific themes. This is underway. This coming week, the National Assembly will again cast its vote on the budget, following its review by the parliamentary commissions. This last step is largely pro forma.

In practice, this means that the true political decisions are made at this stage, within the various parliamentary commissions. The process is relatively opaque, which gives politicians some leeway to do their job. Negotiations are often disguised as technical arguments, with each party using an army of lawyers to bring some credibility to what is largely a political debate.

PS, the main opposition party, has put forward several proposals which are small and have no real economic impact on investors or economic growth. Sentiment seems to be that PS does not really have any alternatives to the austerity measures which are being put forward by Government.

Yet there are alternatives. While the 2013 budget was largely about raising taxes and getting more income to service debt, this one is about cuts in expenditure. The cuts are being carried out essentially via reductions in wages and pension obligations. Very little is being done to improve the efficiency of Government’s consumption. Specifically, Government could use electronic procurement platforms to optimise public spending. The gains in efficiency could be real. Various proposals have been put forward in this direction, none of which seem to have been taken into account.

This budget represents another lost opportunity to improve the State’s efficiency. The Portuguese State is like a huge tanker which follows its course. Trying to steer it takes extremely long and the only way to reduce costs seems to be via cuts in wages and pensions. Any attempt to improve its efficiency seems to be futile.

A common question in today’s market and business environment is whether R&D investment translates into a profitable and marketable solution or product. This question is addressed in a recent Booz & Company survey, which maps the efficiency of R&D investment against the ability of each company to market goods and services.

One of the facts that stand out in the survey is that Apple, one of the main examples of transforming innovative ideas into marketable products, spends roughly 2.2% of sales on R&D, well below the industry average of 6.5%. This is another example of the lack of correlation between investment in R&D and the development of marketable products.

The survey also reveals that companies that engage customers in order to understand their needs and wants and then try to be first in developing new products that respond to those needs, tend to be more effective in their early-stage innovation efforts.

One of the survey’s main conclusions is the notion that the financial crisis did not slow down R&D investment, as companies are keener to generate profit from new products and ideas. However, successful innovation does not appear to necessarily involve new techniques (e.g. social networking and co-creation, cutting edge physics) just the knowledge of what works and what does not really work in the marketplace.

The chart below shows the effectiveness of innovation (measured as a trade-off between idea creation and conversion):

The effectiveness of innovation can also be measured by the amount of innovation pursuers and GDP % of investment in R&D. The chart below shows the tendencies of this indicator for OECD countries.

Finland is the country with the highest number of scientists and engineers and higher percentage of R&D investment. Israel is an interesting case, as the country invests heavily in R&D yet does not need a high number of scientists in order to do so – an example of efficiency. At the other end of the spectrum is Greece, which produces a high number of scientists yet does not invest in R&D.

How much will European economies grow in the medium term (3-5 years)?

Different quarters will answer in totally different ways at present. If you are talking with a politician, the answer will probably be that, following a period of austerity and deficit reduction, Europe will be back to growth.

Analysts and investors will likely give you a different answer. Everyone is talking about the so-called muddle-through economy. Few analysts expect a period of sustained growth in Western Europe before 2020.

These different views will be the source of many difficulties in the coming years. It is very likely that politicians will continue to over-promise until the political class itself realises that the muddle through scenario is, in fact, most likely to happen.

This is all to do with types of innovation. Clayton Christensen wrote about types of innovation in a recent article (see link below) and mentions three broad categories: empowering innovations (think Ford T), sustaining innovations (think Toyota Prius) and efficiency innovations (online banking). While the first type of innovation involves building huge factories to bring new products to the masses, thus creating jobs, the second type is neutral (in Christensen’s example, Toyota sells less Camrys as it increases its Prius sales) and the third type destroys jobs (your bank will employ fewer cashiers if customers prefer to bank online).

Sustaining innovation (Photo credit: Wikipedia)

Europe’s economy is all about sustaining and efficiency innovation at present. This means moderate economic growth and persistently high unemployment. We just need to adapt to this new reality. It will impact the way we work and live.

Portuguese companies have suffered a downturn in their financial stability ever since start of the crisis in 2008. Company insolvencies have now reached a number of around 15,000 since the beginning of 2012, which accounts for 50 new insolvencies per day, as reported in newspaper Público. Looking at the historic company insolvencies in Portugal below, 2008 was the most dramatic period with 41,245 insolvencies. This statistic (total insolvencies) is not directly comparable with the 50 insolvencies per day figure for a number of reasons. It is likely that the total number of insolvencies in 2012 will show an increase on the previous year.

Source: PorData

Consultants Euler-Hermes expect a 50% increase in insolvencies in Portugal this year, as shown below. This is well above other European countries, including Spain and Greece.

Source: Euler-Hermes August 2012 Report

According to the August 2012 Report by Euler-Hermes, in Portugal “there is a time gap between the economic policy decision and its impact on the real economy. The industrial fabric is in danger and rebuilding it will take some time”.

This recent wave of company insolvencies is but a symptom of the adverse financial conditions that most Portuguese companies are facing. Between the Government’s austerity measures and the slowdown in Spain, one of the country’s major trading partners, companies are facing major headwinds.

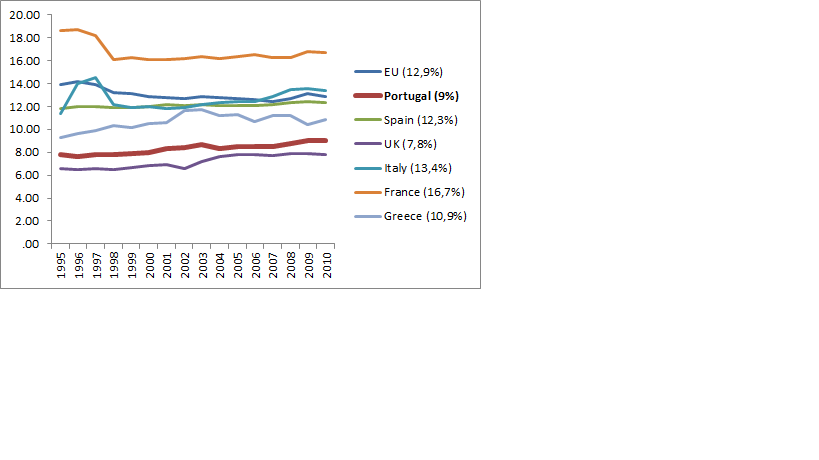

In our view, the answer is to invest in innovative projects. Companies facing financial difficulties are less likely to take on new projects however we believe that this is exactly what the economy needs. Below is a chart of the percentage of GDP invested in R&D for Portugal and other European countries. Germany is an example of economic development. In Germany, R&D spend represents almost 3% of GDP. While Portugal has increased its share from 0.7% in 2005 to 1.6% in 2010 and is well above countries such as Greece or Spain, that trend is reversing. R&D spend is just a proxy for innovation however, a reduction of R&D spend does not bode well for a future economic recovery.

Reactions to withdrawal of the proposed changes in social security contributions

We think it is relevant to do a quick analysis on the aftermath of the initial announcement of proposed changes to social security contributions and the corresponding investors’ reactions. The Portuguese government bond yields (10 year maturity) reacted negatively to the announcement and subsequent withdrawal of proposed changes to social security contributions. Yields have been increasing almost continuously since 7 September, the date of the initial announcement of the proposed changes by the Prime Minister.

The yields in 10-year Government bonds react to a number of factors, aside from internal policy developments. Investors may be reacting to events taking place in Spain. However, investors have almost certainly detected that the current Government has lost momentum as it announced proposed changes to the social security contributions and then had to pull back in haste following a widespread negative reaction to the proposal.

Portuguese Government Bond Yield (10 Y)

Source: Bloomberg as at 1 October 2012

These themes were discussed in ETV’s “Closing Bell” programme on 2 October (in Portuguese):

On 7 September 2012, the Portuguese Government announced new austerity measures that include an increase (of 7 percentage points) in the contribution of workers towards social security together with a decrease (of 5.25 percentage points) in the contribution of companies. This would place Portugal broadly in line with Germany. The first measure was aimed at fighting the increased cost with social security and generally to help achieve the new deficit goal, agreed with the ECB, EU Commission and IMF. The second measure taken was aimed at providing companies with sufficient funds (savings from the tax break) to keep jobs and foster employment.

Impact on the economy

This measure should help support the social security accounts that are suffering badly from the rise in unemployment. Moreover, the Government expects that this measure will support employment and increase competitiveness for firms (according to finance minister Vitor Gaspar, this measure will create 1 to 2% employment by 2015), as a result of lower costs for employers. However, these effects are unlikely to have a significant impact in the short run. A recent study by four economists from the University of Minho revealed that the net effect of measures will actually increase the unemployed by 68 thousand. The economic outlook remains sharply recessionary for Portugal, and cloudy for most of Portugal’s trading partners. This scenario is not favorable for the predictions made by the government.

Reactions

Reactions to the announcement of these austerity measures were widespread and predominately negative. In Portugal, business leaders rose against the measures saying they were unnecessary and will not benefit their companies. Paulo de Azevedo from Sonae, one of the largest business groups in Portugal, claimed that these measures would be harmful for non-exporting companies. The announcement also shook the political sphere with the opposition and even some members of the Government party (PPD/PSD) opposing and criticising the measures. The coalition that enabled the government to have majority in the Portuguese parliament was weakened with the head of CDS/PP publicly admitting to be against the measures.

Source: Bloomberg

Investors’ reaction was ambiguous or indifferent as we can see that from the chart above. It shows the yield to maturity of Portuguese 10 year government bonds and its evolution last month. The first drop which occurred on 5 of September was an obvious positive reaction to the ECB’s announcement of its intention to purchase sovereign debt from struggling countries. However, the reaction after the announcement of these measures (on 7 September) was negative, at first glance. However, it is hard to isolate the effect, due to a high number of relevant events that might have also affected the yield. It is unclear whether the markets are factoring in one of the largest demonstrations in the history of the country having taken place during the weekend.

The European Commission admitted that the government could drop the measures if it could come up with an alternative to fulfill the adjustment programme’s goals as agreed with the IMF. A year ago, IMF representatives alerted to the risks of these measures and their intended purpose. The delegates believed that “it is not obvious that promoting employment is a good substitute for increased efficiency”. Moreover, the head of the IMF delegation, Adebe Salassi, recently stated that these measures were not enforced by the delegation and were solely an initiative of the Portuguese government.

As these measures are likely to affect the contributions to social security in Portugal, we find it relevant to compare these with other European countries. Looking at the overall map of aggregate contributions of employees and employers for the European Union countries as a percentage of GDP until 2010, we find that Portugal is below other countries in terms of contributions and is closer to the UK than to other southern European countries such as Spain or Italy, for example.

Source: Eurostat

Innovation Models insight

Here at innovation models, our opinion/reaction about this measure is also mixed. Had Government announced that the proceeds from the reduction in employer contributions were directed at developing innovative projects that might foster employment in the long run, we would consider these measures as positive. This would have been difficult to implement anyway. We believe that the source of the economic difficulties in Portugal has not been addressed yet.

This matter was discussed in ETV’s “Closing Bell” programme on 18 September (in Portuguese):

Debt of non-financial private companies in Portugal as a % of GDP, 2009-2013. Source: Bank of Portugal (2014)

Debt of non-financial private companies in Portugal as a % of GDP, 2009-2013. Source: Bank of Portugal (2014) Sources of financing for a sample of start-ups based in Lisbon (2014). Source: Macrometria

Sources of financing for a sample of start-ups based in Lisbon (2014). Source: Macrometria

{kind=link}

{kind=link}